The Digital Net Tightens: How Radar-FVA Integration is Transforming Road Enforcement in 2026

Since February 16, 2026, the landscape of French road safety has undergone a silent but profound technological shift. Automated speed cameras, once strictly the domain of traffic speed enforcement, now serve as a primary tool for verifying administrative compliance. Specifically, when a vehicle is caught in a "major speeding" event—defined as an excess of 50 km/h or more over the legal limit—the system now automatically cross-references the vehicle’s license plate against the Fichier des Véhicules Assurés (FVA, or the File of Insured Vehicles).

This integration marks a critical step in the French government’s ongoing campaign to eliminate uninsured driving. With the disappearance of the physical "green insurance sticker" on April 1, 2024, the FVA has become the sole legal proof of insurance. Today, a failure to appear in this database during a speed enforcement event triggers a dual-sanction mechanism that carries heavy financial and legal consequences.

The Mechanics of the FVA-Radar Cross-Check

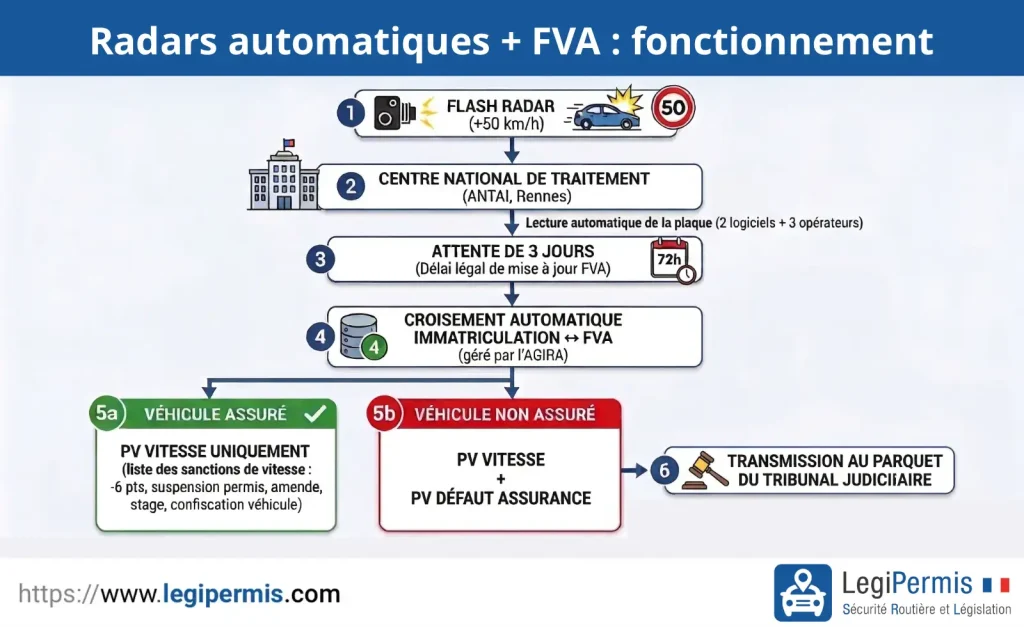

The operation is seamless and instantaneous. When a fixed, mobile, or onboard radar captures an image of a vehicle traveling at least 50 km/h above the speed limit, the registration data is transmitted to the National Processing Center (CNT) in Rennes.

Following a mandatory three-day grace period—aligned with the legal requirement for insurers to update the FVA database—the system performs an automated check against the AGIRA (Association for the Management of Information on Insurance Risk) database. If the vehicle is absent from the FVA, the breach of insurance law is flagged alongside the speeding violation. This initiates a simultaneous legal process where the driver is held accountable for both the dangerous driving act and the administrative failure to carry mandatory civil liability insurance.

Why the 50 km/h Threshold?

Critics and observers have questioned why this enforcement is currently limited to "major" speeding violations. According to the Interministerial Committee for Road Safety (CISR), the threshold is a calculated policy choice rather than a technological limitation. The rationale is three-fold:

- Deterrence of High-Risk Behavior: The government aims to target the most reckless drivers, who statistically represent the highest danger to other road users.

- Data Reliability: By focusing on high-speed infractions, the system ensures that the legal case built against the offender is robust and less prone to administrative contestation.

- Phased Implementation: The authorities are testing the load capacity of the FVA-CNT interface to ensure system stability before potentially expanding the scope of enforcement.

Verifying Your Status: A Step-by-Step Guide

With the physical insurance certificate now obsolete, it is the responsibility of every vehicle owner to ensure their insurance company has properly transmitted their data to the FVA. You can verify your status through three official channels:

- The Online Portal (fva-assurance.fr): This is the most direct method. By entering your vehicle’s registration number and the "formula number" found in section C.4.1 of your vehicle registration certificate (carte grise), you can see if your vehicle is recorded, the name of your insurer, and the validity period.

- The Voice Server: For those who prefer telephone assistance, the service at 01 83 64 32 22 provides real-time verification during business hours.

- Direct Contact with Your Insurer: If you have recently subscribed to a policy, request a Mémo Véhicule Assuré (MVA). This document serves as proof of insurance for 15 days, allowing time for the information to propagate through the central database.

What to do if you aren’t in the system?

If your vehicle does not appear in the FVA, do not panic, but act immediately. If you have subscribed to insurance within the last 72 hours, simply wait; the lag is usually due to the processing time of the insurance company. If you have recently switched insurers, contact your new provider to ensure they have sent the update to AGIRA. For those who have purchased a used vehicle, remember that the obligation to insure begins the moment the sale is finalized.

The Financial and Legal Stakes

The consequences of being caught for both a major speeding violation and a lack of insurance are severe. The "double sanction" is designed to hit both the wallet and the driver’s legal standing.

Breakdown of Potential Sanctions

| Infraction | Fixed Penalty (Initial) | Maximum Tribunal Penalty |

|---|---|---|

| Major Speeding (≥ +50 km/h) | €300 | €3,750 + 3 months prison |

| No Insurance (1st offense) | €500 | €3,750 |

| FGAO Contribution | €250 | N/A |

| TOTAL MINIMUM | €1,050 | €7,500+ |

Beyond the fines, the tribunal can impose accessory penalties, such as the confiscation of the vehicle, a suspension of the driver’s license for up to three years, or a mandatory road safety training course. It is important to note that while the speeding infraction triggers a six-point penalty on your license, the failure to insure does not result in a point deduction—though it opens the door to far more significant criminal proceedings.

The "Time Bomb": Accidents Without Insurance

While administrative fines are significant, they pale in comparison to the financial ruin associated with an accident involving an uninsured vehicle. If a driver is responsible for an accident, the Fonds de Garantie des Assurances Obligatoires (FGAO) compensates the victims. However, under French law, the FGAO is legally obligated to recover these funds from the responsible driver, plus a 10% penalty.

In cases of serious bodily injury, these debts can reach hundreds of thousands of euros. Statistics from 2024 indicate that over 15,400 individuals were indebted to the FGAO, with many facing lifetime repayment plans. The FGAO paid out €123 million in damages in 2024 alone, highlighting the systemic risk posed by the approximately 515,000 uninsured drivers currently on French roads.

Data and Trends: Who is Driving Uninsured?

According to the 2025 Barometer of Road Non-Insurance, the profile of the typical uninsured driver is often younger, lower-income, or experiencing a transitionary period (e.g., job loss or recent move). Despite representing a small percentage of the total driving population, uninsured drivers are involved in roughly 4.8% of all bodily injury accidents—a figure that has doubled over the last decade.

Key Data Points:

- Mortality Risk: Drivers of uninsured vehicles are four times more likely to be involved in a fatal accident than their insured counterparts.

- Economic Burden: Less than 10% of the funds paid out by the FGAO are successfully recovered from the guilty parties, creating a massive deficit that is ultimately subsidized by the premiums of insured drivers.

- Regional Disparities: Urban areas with lower socioeconomic stability show higher concentrations of uninsured vehicles, often linked to the rising costs of insurance premiums for high-risk vehicles.

Future Outlook: A Broader Net?

While the current radar-FVA enforcement is limited to extreme speeding, many observers anticipate a future expansion. There are ongoing discussions about incorporating the FVA check into all radar flashes, including minor speeding offenses. Proponents argue this would be the most effective way to eliminate uninsured driving entirely.

However, this proposal faces significant pushback regarding civil liberties. Privacy advocates and the CNIL (the French data protection authority) have raised concerns about the proportionality of using traffic enforcement tools for systemic administrative surveillance. Transforming every speed camera into a permanent checkpoint for insurance compliance would represent a significant expansion of the state’s monitoring power.

As of early 2026, no official calendar for such an expansion has been released. The government remains focused on stabilizing the current system, ensuring that the interface between the CNT and the FVA is flawless before considering further integration. For now, the message to drivers is clear: check your insurance status, keep your registration updated, and drive within the limits. In the era of digital surveillance, the price of non-compliance has never been higher.