Insurance Costs: Electric vs. Gasoline Vehicles in 2026 – A Comprehensive Analysis

Are you standing at the crossroads of your next vehicle purchase, debating between the sleek silence of an electric vehicle (EV) and the familiar reliability of a gasoline-powered car? Or perhaps you are a current EV owner startled by your most recent renewal notice. If so, you are not alone. As of 2026, the landscape of automotive insurance in France—and across much of Europe—has undergone a historic shift. For the first time, insuring an electric vehicle has become consistently more expensive than insuring its internal combustion engine (ICE) counterpart.

This article provides an in-depth exploration of why this inversion has occurred, what the current figures tell us, and what this means for your personal finances as we navigate the automotive transition.

The Core Data: Quantifying the Gap in 2026

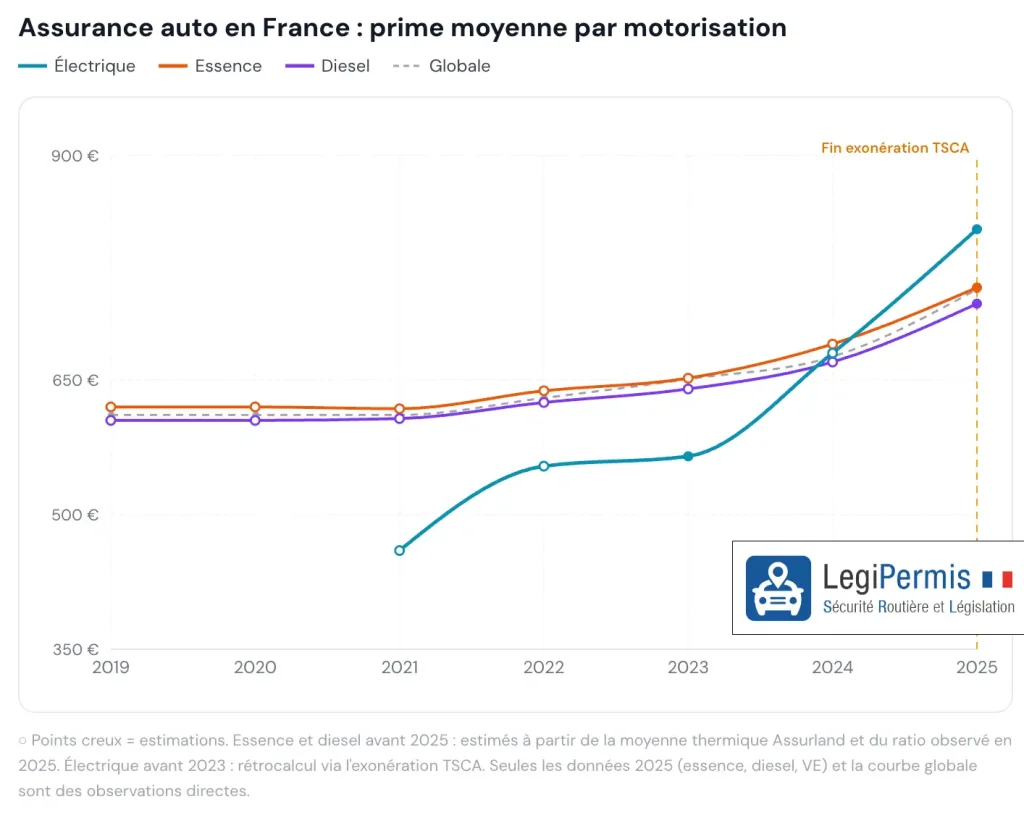

The narrative that electric vehicles are cheaper to maintain and operate is being challenged by the reality of insurance premiums. According to data aggregated from major market barometers in early 2026, the average annual premium for an electric vehicle now sits between €793 and €818. In contrast, owners of gasoline-powered vehicles are paying between €684 and €753.

This represents a notable price gap of between 9% and 16%, depending on the provider and the specific vehicle profile. To put this into perspective, we must look at the trajectory of these costs over the last three years. In 2023, the situation was the inverse: insuring an EV was roughly €80 cheaper than a thermal vehicle. Today, EV insurance premiums have surged by approximately 45% since 2023, while gasoline and diesel premiums have seen only moderate, inflationary increases.

Comparative Table: Annual Insurance Premiums (2026)

| Vehicle Type | Average Annual Premium (2026) | Evolution Since 2023 |

|---|---|---|

| Electric | €793 – €818 | +45% (vs €565 in 2023) |

| Gasoline | €684 – €753 | Moderate Increase |

| Diesel | ~€735 | Moderate Increase |

Source: Aggregated data from industry analysts (e.g., Assurland).

A Chronology of the Shift: From Incentive to Reality

The transition of EV insurance from a "green-discounted" product to a "premium-priced" one did not happen overnight.

- 2023: The Golden Age of Incentives. At this stage, electric vehicles were favored by regulators and insurers alike. Lower maintenance requirements and perceived lower risks made them attractive.

- 2024: The Gradual Adjustment. Regulators began to phase out fiscal advantages. The total exemption from the Taxe Spéciale sur les Conventions d’Assurance (TSCA) was reduced to 75%. Simultaneously, claims data began to show that while EVs had fewer accidents, the ones they did have were becoming exponentially more expensive to resolve.

- 2025: The Fiscal Cliff. As of January 1, 2025, the remaining TSCA exemptions for new contracts were fully abolished. This tax alone, which accounts for 33% on civil liability and 18% on damage coverage, caused a mechanical, immediate jump in premiums.

- 2026: The New Normal. The market has stabilized at a higher price point, with insurers now pricing in the long-term technical realities of battery repair, weight-related collision damage, and the scarcity of specialized repair facilities.

Why the Surge? The Mechanics Behind the Costs

To understand why your premiums have risen, one must look at the technical and fiscal factors that insurers are now passing on to the consumer.

1. The Erosion of Fiscal Advantages (TSCA)

The most significant driver of the recent hike is the elimination of the TSCA. Until 2023, EVs were exempt from this specific tax, which serves as a major source of revenue for the state. By removing this exemption, the government essentially added a "tax premium" to every EV insurance policy. Estimates from the Mutuelle Fraternelle d’Assurances (MFA) suggest that without this fiscal change, the increase in EV insurance would have been closer to 6%, consistent with the broader automotive market. Instead, the tax change alone accounted for a 20% jump.

2. The High Cost of Repairs

Electric vehicles are technologically complex. According to the 2024 Observatoire SRA (the reference body for automotive claims), EVs cost 14.3% more to repair than the average vehicle in the fleet, with hybrid vehicles trailing closely behind at +15.7%.

- Parts Inflation: The cost of spare parts for EVs has risen by 29% since 2020.

- The "Replace vs. Repair" Dilemma: SRA reports indicate that 72% of parts in an EV accident are replaced rather than repaired. This is partly due to the delicate nature of electronic sensors and high-voltage components.

- France Assureurs’ Findings: A November 2025 study of 1.9 million vehicles confirmed a massive 28% increase in costs related to "glass breakage" (often involving advanced sensors embedded in windshields) and an 11% overall increase in claims indemnification.

3. The "Battery Risk" Factor

The battery is the heart of an electric vehicle, representing 30% to 50% of its total value. A replacement can cost between €8,000 and €20,000. Alarmingly, France Assureurs notes that only half of current manufacturers provide a pathway for individual module repairs. A relatively minor impact to the undercarriage can lead to a "total loss" classification, as the risk of fire or cell degradation makes insurers hesitant to authorize repairs.

Furthermore, EVs are significantly heavier than their thermal counterparts (an average increase of 41%). In the event of a collision, this additional mass increases the kinetic energy involved, leading to more structural damage and, consequently, higher repair bills.

Perspectives from Abroad: Is This a French Phenomenon?

The challenges facing the French market are reflected globally, though the maturity of each market changes the impact:

- United Kingdom: The UK saw an insurance gap between EVs and thermal vehicles of 39% in early 2024. However, thanks to the maturation of the repair sector, this has narrowed to 10–20% by late 2025. The Association of British Insurers (ABI) notes that repair costs remain 25% higher for EVs, but the gap is closing as workshops gain expertise.

- Germany: The GDV (the German Insurance Federation) reports that while EVs declare 20% fewer accidents, each accident is 25% more expensive. Consequently, German "Vollkasko" (comprehensive) premiums remain 15–25% higher for EVs, a trend that has remained steady throughout 2025.

Counter-Arguments: The Nuances of the EV Profile

Despite the higher premiums, it is essential to look at the full picture. There are several factors that favor the EV owner:

- Reduced Theft Risk: Electric vehicles are equipped with sophisticated, factory-integrated GPS and advanced connectivity. This makes them significantly harder to steal and easier to recover, leading to lower theft-related claims.

- Driving Habits: Demographic data suggests that EV owners tend to drive more cautiously and generally take shorter, urban-centric trips.

- Coverage Bias: It is important to note that 88% to 93% of EV owners choose "all-risk" insurance, compared to only 44–54% for gasoline car owners. This statistical skew makes the average EV premium look higher, as it includes more comprehensive coverage than the average gasoline policy.

Future Outlook: Will the Gap Close?

The current insurance premium gap is not necessarily permanent. Several factors suggest a future convergence:

- Falling Battery Costs: Battery prices have dropped from $400/kWh in 2012 to roughly $115/kWh by the end of 2024, with projections falling toward $80/kWh by 2026. This reduces the "total loss" risk.

- Increased Repair Competency: As more mechanics receive specialized training for high-voltage systems, the reliance on expensive "official manufacturer repairs" will decrease, allowing for more competitive pricing in the aftermarket.

- Repairability Indices: Organizations like France Assureurs are working on a "Repairability Index." By pressuring manufacturers to design cars that are easier and cheaper to fix, the industry hopes to lower the long-term insurance burden.

Practical Advice: How to Optimize Your EV Insurance

If you are currently looking to insure an electric vehicle, don’t just accept the first quote. Follow these strategies to mitigate the costs:

- Compare Before You Buy: Use online comparison tools to check premiums before signing a vehicle purchase contract. A Renault Zoe may cost significantly less to insure than a Tesla Model 3 due to differences in repair costs and parts availability.

- Shop Around for EV-Specific Offers: Many insurers have introduced "Electric Bonus" packages. These may offer lower premiums, specialized assistance for charging station failures, or specific coverage for the battery pack.

- Consider Telematics ("Pay-as-you-drive"): If you are a low-mileage driver, take advantage of the fact that EVs are already connected. Insurance policies that track your mileage can result in significant annual savings.

- Audit Your Coverage: Ensure that your battery is explicitly covered in your contract, especially if you are in a leasing (LOA/LLD) agreement. Some basic policies exclude the battery if it is not owned by the driver, which could leave you financially exposed in an accident.

Conclusion

While the "green transition" has hit a bump in the road regarding insurance costs, the current 9% to 16% surcharge for electric vehicles is largely a result of structural market adjustments—specifically the loss of tax exemptions and the infancy of the specialized repair ecosystem. As the technology matures and the automotive industry continues to standardize EV production, these costs are likely to normalize. For now, being a savvy consumer—comparing quotes, choosing a repair-friendly vehicle, and understanding your coverage—remains the most effective way to enjoy the benefits of electric mobility without breaking the bank.