Auto Insurance in 2026: A Deep Dive into Rising Premiums and Strategic Savings

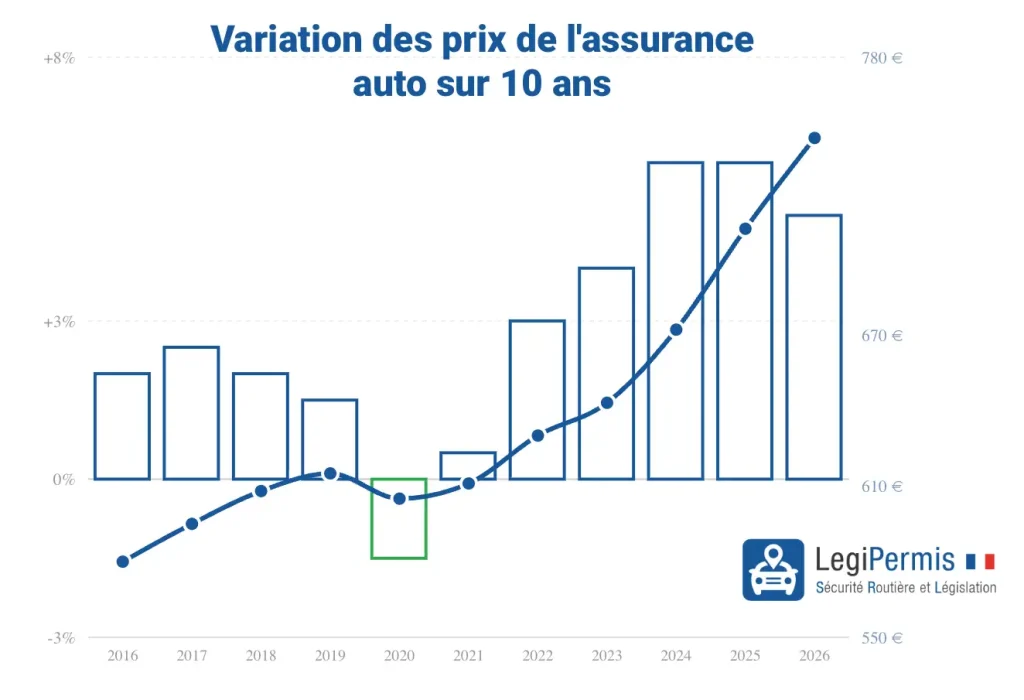

For the third consecutive year, European motorists—and specifically those in France—are facing a relentless climb in automobile insurance premiums. As we navigate through 2026, the cost of coverage has surged by an additional 4% to 6%, translating to an average annual increase of €30 to €50 for standard contracts. For younger drivers, the financial burden has reached a breaking point, with average premiums now exceeding €2,100 annually.

This is not a temporary market fluctuation, but rather the result of a convergence of economic, technological, and climatic pressures. Understanding these mechanisms is the first step for any policyholder looking to navigate this difficult fiscal landscape.

The Core Facts: Why Premiums Are Climbing

The 2026 insurance crisis is multifaceted. While the pace of growth has slowed slightly compared to the sharp spikes of 2023 and 2024, the cumulative effect is significant. A contract that cost €500 just three years ago can now exceed €580.

1. The Soaring Cost of Repairs

The primary driver of these increases is the rising cost of vehicle maintenance. According to data from the SRA (Security and Automobile Repair), the cost of repairs increased by 7.9% in 2024 and maintained a 6% growth rate throughout 2025.

Several factors contribute to this:

- Technological Complexity: Modern vehicles are equipped with advanced driver-assistance systems (ADAS), high-definition cameras, and sophisticated sensors. A simple bumper collision no longer just requires bodywork; it necessitates recalibration of electronic systems, driving up labor and parts costs.

- Parts Inflation: Spare parts now account for more than 50% of the total cost of an average repair. As manufacturers consolidate supply chains and prioritize proprietary parts, the cost of replacements has ballooned.

2. The Electric Vehicle (EV) Premium

2026 marks a turning point for the electrification of the road. The previous tax advantages that shielded EVs from certain levies have been phased out. The TSCA (Special Tax on Insurance Conventions) now applies equally to internal combustion engines and electric vehicles.

Because electric vehicles often involve more expensive, specialized components and require technicians with specific high-voltage certifications, the cost to insure these vehicles remains high. Owners who once enjoyed subsidies are now facing the full weight of market-rate insurance, with some high-performance models seeing premium hikes that outpace their gas-powered counterparts.

Chronology of the Insurance Crisis

To understand the current state of the market, one must look at the recent historical trajectory of insurance premiums:

- 2023: The beginning of the cycle. Inflationary pressures post-pandemic began to impact global supply chains, causing the first significant jumps in premiums (approx. +3-4%).

- 2024: A year of structural adjustment. Repairs became significantly more expensive, and insurers began to account for the increased frequency of high-cost climatic events.

- 2025: A "perfect storm" year. Major climate events led to over €2 billion in damages, and the government mandated an increase in the "CatNat" (natural disaster) surcharges to address the bankruptcy risk of the national disaster fund.

- 2026: Consolidation of high costs. While the industry is attempting to stabilize, the combination of high repair costs and increased climate risk ensures that premiums remain elevated.

Supporting Data and Climatic Implications

The role of climate change in insurance pricing cannot be overstated. The year 2025 was a watershed moment for the industry, marked by severe droughts, massive flooding, and wildfires.

According to France Assureurs, the projected cost of natural disasters is expected to hit a staggering €143 billion by 2050. Because insurance is a system of mutualization, the cost of these disasters is spread across the entire policyholder base. Even drivers living in areas not directly impacted by recent floods are seeing their premiums rise to cover the massive payouts in high-risk zones.

Furthermore, the government-mandated "CatNat" surcharge increased from 6% to 9% on January 1, 2025. This move, intended to inject €1.2 billion annually into the CCR (Central Reinsurance Fund), was necessary to rescue a fund that had been in deficit since 2015.

Official Responses and Industry Outlook

Insurance companies argue that they have little choice but to pass these costs onto the consumer. The rising frequency of severe accidents and the increased severity of injuries reported by the ONISR (National Inter-ministerial Observatory for Road Safety) have created a high-risk environment.

The insurance sector is currently focusing on "risk segmentation." This means that algorithms are becoming increasingly precise in calculating the probability of a claim. High-risk drivers—those with multiple minor incidents or those living in urban centers with high theft rates—are seeing the sharpest increases, while low-risk, experienced drivers with clean records are being "rewarded" with more moderate, though still present, increases.

Implications for the Modern Motorist

The changing landscape of 2026 forces a shift in how individuals approach their insurance contracts. The "set it and forget it" mentality is now a financial liability.

Who is most affected?

- Young Drivers: The high cost of insuring novice drivers is being exacerbated by the general market rise, pricing many out of vehicle ownership.

- Urban Residents: Higher traffic density leads to more minor collisions, resulting in higher risk profiles for city dwellers.

- Owners of Premium Tech Vehicles: Cars loaded with expensive sensors and safety features are more costly to repair, leading to higher insurance premiums.

Strategic Ways to Reduce Your Premium

Despite the structural nature of these hikes, consumers are not powerless. By taking a proactive approach, many can mitigate or even reverse the impact of these increases.

1. Leverage the Law for Competitive Shopping

The "Hamon Law" remains your most powerful tool. It allows you to terminate your contract at any time after the first year without penalty. Use this to shop around annually. Differences in premiums between companies for the same driver profile can reach 40%. Digital-first insurers and neobrokers often have lower overheads and are more aggressive in their pricing to capture market share.

2. Audit Your Coverage

Do you really need comprehensive coverage (Tous Risques) for an aging vehicle? If your car’s market value has depreciated significantly, switching to "Third Party Plus" (Tiers étendu) can save you a substantial amount of money each year.

3. Adjust Your Deductibles (Franchise)

If you have a strong driving history and an emergency fund, consider increasing your deductible. By agreeing to pay a higher out-of-pocket cost in the event of a minor claim, you can significantly lower your monthly premium.

4. Optimize Based on Usage

- The Kilometer Limit: If you work from home or use public transport, opting for an "at-the-kilometer" contract can save you 20% to 30%.

- Garage Parking: If you have access to a private, closed garage, declare it. Insurers offer lower rates for vehicles that are protected from theft and vandalism.

- Safety Features: Many insurers offer discounts for vehicles equipped with autonomous braking, lane-keep assist, or advanced dashcams. Ensure your insurer is aware of every safety feature your car possesses.

5. Check the Repairability Index

Before your next vehicle purchase, consult the SRA’s repairability index. Choosing a model that is easy and inexpensive to repair is a long-term investment that will pay dividends in lower insurance premiums for as long as you own the vehicle.

Conclusion

The insurance market in 2026 is defined by a "new normal" of higher costs, driven by a combination of technological progress, climate instability, and the necessity of maintaining a solvent risk-pool. While the upward trend is unlikely to reverse, the informed motorist can navigate these waters by exercising their right to switch providers, optimizing their coverage levels, and making smart choices regarding their vehicles. In an era of rising costs, financial literacy regarding your insurance policy is not just a benefit—it is a necessity.